- Nationwide, 19% of Black households are cost-burdened, compared to 12% of white households, 17% of Hispanic households and 18% of Asian households.

- The value of Black-owned homes has declined more than the value of homes owned by other racial groups, with a 0.7% drop during a year in which home values have remained mostly flat.

- Recent trends contribute to ongoing racial disparities in housing.

A new Zillow analysis of 2023 data (the most recent data available) finds that minority homeowners are more likely to be cost-burdened nationwide.

The cost burden has worsened for Black households over a five-year period, while it has improved or held steady for other groups. Nationwide in 2018, only 17% of Black households were cost-burdened, compared with 19% of Asian households, 18% of Hispanic households and 12% of white households.

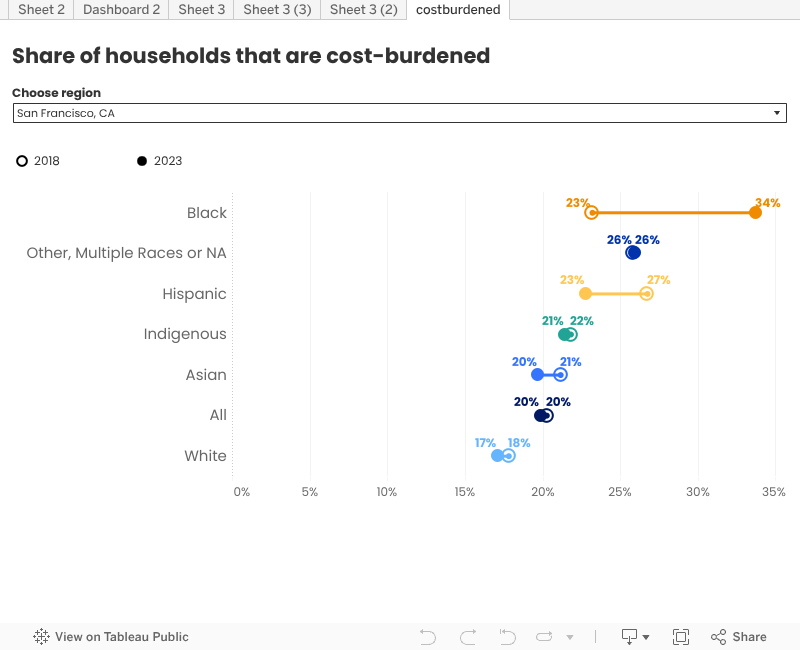

Black households face some of the heaviest burdens in three expensive California markets, shouldering disproportionately high housing costs among homeowners.

- San Francisco: 34% of Black households are cost-burdened, compared to 17% of white households, 20% of Asian households and 23% of Hispanic households.

- Riverside: 32% of Black households are cost-burdened, compared to 21% of white households, 22% of Hispanic households and 26% of Asian households.

- Los Angeles: 30% of Black households are cost-burdened, compared to 22% of white households, 23% of Hispanic households and 24% of Asian households.

Today, fewer than half of Black households own their homes. The rapid rise of home values during the pandemic, coupled with the doubling of mortgage rates, may be preventing more Black people from buying homes. Moreover, 54% of Black renters are cost-burdened — the highest share of any racial group — which makes it more difficult to save for a down payment.

Black households also face roadblocks in securing a loan: 25% of Black applicants were denied a mortgage for a primary home purchase in 2023, compared to 11% of white applicants. The top reasons for denials among Black applicants were credit history and debt-to-income ratio.

Rising insurance and home-repair costs pose further financial burdens for minority homeowners

For people who successfully buy a home, the financial headwinds aren’t letting up. Since 2019, the cost of homeowners’ insurance has grown at twice the rate of incomes.

Recent research from the Joint Center for Housing Studies (JCHS) at Harvard University also found that improvement and repair costs disproportionately strain Black, multiracial and Hispanic homeowners, reflecting disparities in incomes, savings and home equity, among other things. In 2023, Black households spent an average of 8.3% of their income on improvement and maintenance; Hispanic households spent 7.8%; Asian households spent 6.1%; and white households spent 7.4%. The JCHS report highlights that these higher burdens force homeowners to give higher priority to the critical projects such as replacements and disaster repair.

Regional dynamics slow progress gained in shrinking home value gap

In addition to facing greater cost burdens when it comes to homeownership, Black homeowners are experiencing greater disparities in home values.

Over the past year, home value growth has remained flat nationally. But Black homeowners have seen their home values drop an estimated 0.7% on average. By comparison, Hispanic homeowners saw their home values decline by 0.2%, and home values of Asian households and white households essentially held steady, witnessing a rise of 0.1%.

Looking further back in time, home values have risen significantly since the beginning of the pandemic. Still, home values for minority households continue to lag behind those of white households.

Zillow has retraced the progress made from 2020 to 2022 to close the home value gap. Compared with white-owned homes, Black-owned homes were typically valued 15.7% lower in February 2020. That gap narrowed to 13.9% lower in June 2022, but has widened to 15.1% lower as of August 2025. For Hispanic-owned homes, the gap narrowed from 9.4% lower in February 2020 to 9% at its July 2024 low. It then widened to 9.2% in August 2025.

The geography of this retracement reflects where pandemic demand has cooled the most. For Black homeowners, the largest declines are concentrated in the Midwest and the South, where home values have slipped faster than the national average. Strains on housing affordability and slower job growth have weighed heavily on those areas as well. For Hispanic homeowners, the main driver has been the relative softening of home values in parts of the South and Southwest, which is a sharp reversal from the skyrocketing appreciation seen in those areas during the early years of the pandemic.

Among the 50 largest metro areas, Detroit, St. Louis and Cleveland show the largest gaps between Black- and white-owned home values, while Riverside, Portland (Oregon) and Las Vegas post the smallest gaps. For Hispanic homeowners, the largest gaps relative to white homeowners are in Los Angeles, San Jose and Memphis; the narrowest are in Cincinnati, Pittsburgh and Portland.

Despite the challenges, homeownership is still the primary pathway to wealth for most U.S. households — and it plays an outsize role in the overall racial wealth gap. Zillow’s earlier research estimated that about 38% of the median wealth gap between Black and white households is tied directly to differences in homeownership and home values. For the wealth gap between Hispanic and white households, that figure is 24.6%.

The bottom line

Today, Black homeowners are experiencing the brunt of burdens linked to the rising costs of homeownership, the higher risk of natural disaster, the decline in home values and the racial wealth gap.